The Finance Problem Nobody Wants to Talk About

By TED ROSE, ROSE FINANCIAL SOLUTIONS

Over the past two weeks, we covered the first two pillars of financial infrastructure readiness: Structural Foundation and Systems Architecture. Both deal with things that are relatively easy to point to. Controls either exist or they do not. Systems are either connected or they are not. This week is different.

Pillar 3 is Operational Discipline, and it is the hardest pillar to talk about because it is the least glamorous. Nobody walks into a leadership meeting and says, "I want to talk about our process documentation." Nobody wins a client by leading with close management cadence.

But here is what I know after thirty years of building finance infrastructure for growing companies: operational discipline is the difference between a finance function that holds up under pressure and one that quietly falls apart every time the business hits a growth phase, a key departure, or an audit. Everything else we have discussed, controls, systems, reporting, AI readiness, depends on this. And most companies have not built it.

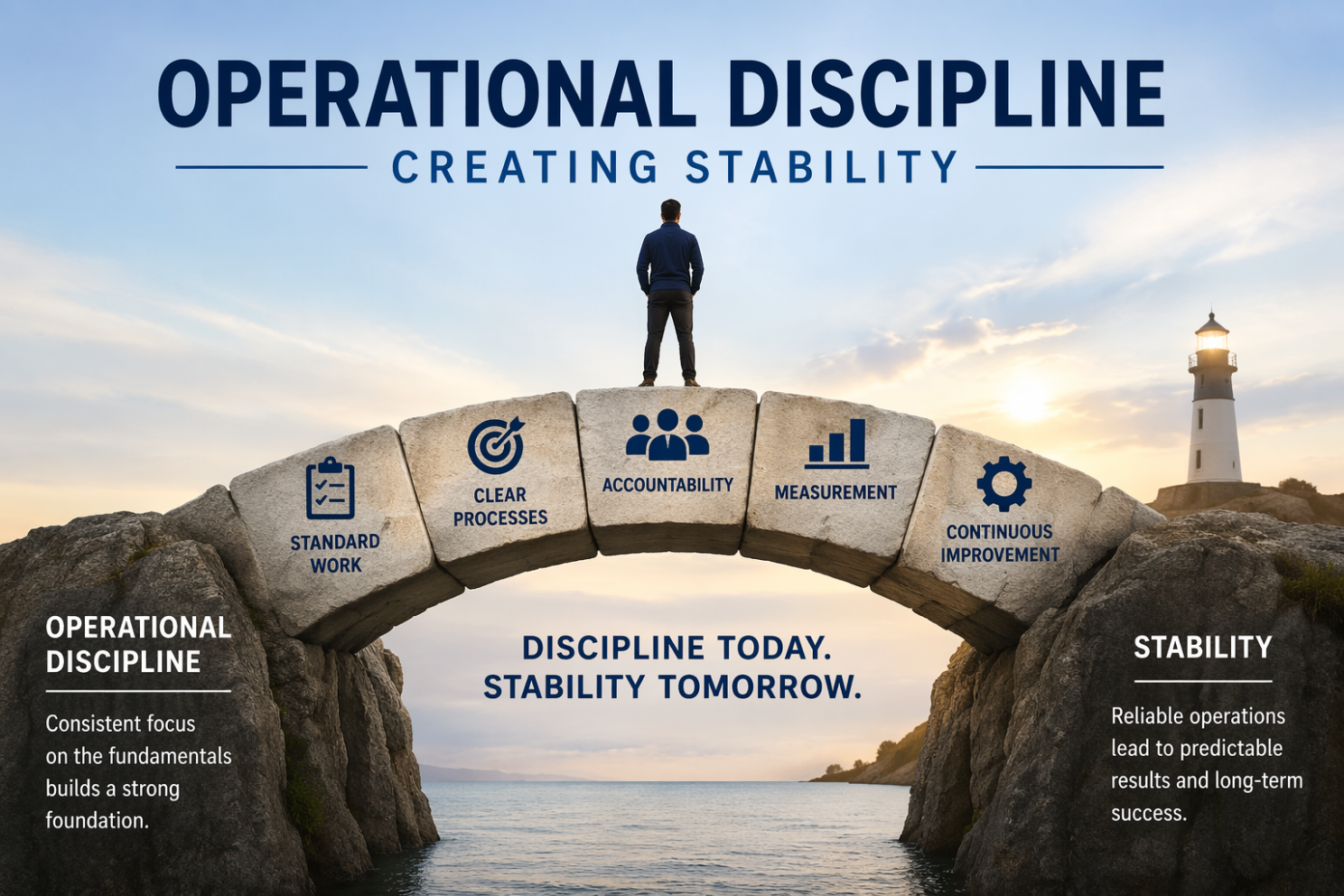

What Operational Discipline Actually Is

Let me be precise, because this pillar gets misunderstood. Operational discipline is not about working harder. It is not about adding more oversight or making the finance team's life more complicated. It is about whether the finance function runs as a system or as a collection of individual efforts held together by a few talented people who carry too much in their heads.

Specifically, it covers four areas.

- Process documentation. Are the workflows, procedures, and close steps written down, current, and accessible? Or do they live in the institutional memory of whoever has been in the seat the longest?

- Workflow ownership. Does every critical finance process have a clear owner, a defined timeline, and an accountable reviewer? Or does it get done when someone gets around to it, with variable quality depending on who is doing it?

- Execution cadence. Does the finance function operate on a consistent, predictable rhythm: close deadlines, budget reviews, cash flow updates, variance analysis? Or does it run reactively, lurching from month-end to month-end?

- Data quality and budget discipline. Is financial data being reviewed and validated as part of a standard process, or corrected after the fact when something looks wrong? Are budgets being tracked and reviewed consistently, or built once a year and forgotten?

- When these four things are in place, the finance function is a system. When they are not, it is a dependency on specific people performing heroics under pressure.

The Problem Most Companies Misdiagnose

When a month-end close runs long, leadership almost always asks the same question: do we need more people? Sometimes the answer is yes. But more often, the real issue is that the process was never designed. It accumulated the same way fragmented systems accumulate. Someone figured out how to do it. It worked. Nobody wrote it down. That person became the only one who could do it reliably. And now the close is hostage to their availability, their memory, and their continued employment. This is not a staffing problem. It is a process design problem.

Adding headcount to an undocumented, inconsistent process does not fix it. It creates more expensive inconsistency. The new hire learns the process the way everyone else did: informally, incompletely, and dependent on whoever trained them.

The same principle applies to budget management, cash monitoring, and variance review. When those activities depend on someone remembering to do them rather than on a defined cadence and a documented process, they become unreliable. Not because the team is careless. Because the system was never built to make them reliable.

The Key-Person Risk Nobody Prices In

I want to spend a moment on this because it is one of the most consistently underestimated risks in growing companies. Finance teams at the $10M to $50M stage tend to be lean. Often there is a CFO or controller who is deeply capable and deeply embedded in how the finance function operates. They know the close process. They know the quirks of the ERP configuration. They know which numbers to watch and which variances to investigate. They are invaluable.

They are also a single point of failure. When that person leaves, which they eventually will, through promotion, departure, health, or any number of other reasons, the institutional knowledge goes with them. What remains is a finance function that cannot close reliably, cannot produce trusted reporting on cadence, and cannot onboard a replacement without significant disruption.

I have seen this play out more times than I can count. A company that looked financially healthy from the outside suddenly cannot produce a clean month-end close. The board notices. The bank notices. Sometimes the auditors notice. The solution is not to hold on to key people tighter. The solution is to build a finance function that does not depend on any single person to operate correctly.

That means documented processes. Defined ownership. Cross-trained teams. A close management system that runs on procedure, not memory. When operational discipline is built correctly, the departure of even a strong finance leader is a transition, not a crisis.

Why This Is a GovCon Requirement, Not Just a Best Practice

In commercial environments, weak operational discipline creates internal pain: slow closes, inconsistent reporting, key-person dependency. That is damaging enough. In government contracting, it creates compliance exposure.

DCAA does not just audit your numbers. It audits your processes. Timekeeping consistency, billing accuracy, indirect cost segregation, and incurred cost submissions all depend on operational discipline being embedded into the daily and monthly rhythm of the finance function.

When processes are informal and depend on tribal knowledge, the audit risk is not theoretical. It is present in every transaction that was posted based on habit rather than documented procedure. Every timesheet that was approved outside of a defined workflow. Every indirect cost that was allocated through a process that exists only in one person's head.

The contractors who perform best in DCAA audits are the ones who can produce, quickly and completely, documentation that shows not just what was done but how the process ensures it is done consistently. That kind of documentation does not exist without operational discipline. It cannot be created the week before an audit. It has to be built into the operating rhythm of the finance function.

What Strong Operational Discipline Enables

Like structural foundation and systems architecture before it, operational discipline is most usefully framed not by what it prevents but by what it makes possible. When it is built correctly, several things shift.

- The close becomes predictable. Not fast because everyone worked harder. Predictable because every step has an owner, a timeline, and a documented procedure. The close runs the same way every month regardless of who is in the seat.

- Quality improves without effort. When processes are documented and consistently followed, errors surface earlier because the review steps are built in. The CFO is not catching mistakes in the final review. The process catches them before the CFO ever sees the file.

- Automation becomes achievable. You cannot automate a process that lives in someone's head. Process documentation is the prerequisite for automation. Every workflow that is documented and consistently followed is a workflow that can eventually be systematized. Operational discipline is not just valuable today. It is the foundation for how the finance function scales tomorrow.

- Talent transitions stop being crises. When processes are documented and owned by the system rather than by individuals, a departure triggers a handoff, not a disaster. The new person learns the documented process. The close runs. The reporting lands on time.

What We See When We Assess It

- Operational Discipline is consistently one of the lowest-scoring pillars when we run the FSRR. That is not because companies are careless. It is because process documentation and execution cadence are never urgent until they suddenly are.

- The most common findings:

- The close process has no written procedure. It exists in someone's head or in a spreadsheet checklist that has not been updated in two years and is not shared with anyone else.

- Budget versus actual reviews happen sporadically. They are on the calendar but get pushed when something more urgent comes up, which means they rarely happen on a consistent cadence.

- Cash management is reactive. The bank balance is monitored, but there is no documented cash flow forecast process, no defined trigger points for escalation, and no standard cadence for reviewing receivables and payables aging.

- Process ownership is unclear. Multiple people touch the close, but nobody owns it. When something goes wrong, it is not clear who is accountable.

What this looks like in practice: A fast-scaling firm came to us not because something had broken, but because their finance leader had the self-awareness to see what was coming. The company had grown from $5M to $15M in two years. The close process had grown with it, but informally.

When we conducted our onboarding review, which we now call the FSRR, we documented more than twenty discrete close steps. Fewer than a third had any written procedure, and nearly all of them were owned by the same person. Once we implemented our team-based approach, key team members could take extended leave and the close still ran on schedule. That outcome was the result of time spent in the prior months building out the documentation, assigning ownership, and implementing a close management system. That is what operational discipline looks like when it is working: resilience that the organization never has to think about because it is built into the process.

The Sequence That Makes Everything Else Work

I want to close with something that applies across all five pillars but is most clearly illustrated here. The path to modern, automated, AI-enabled finance is not a technology decision. It is a sequence. Stabilize first. Address the foundational gaps: controls, governance, compliance posture. Get the structural foundation right. Standardize next. Document the processes, define the ownership, build the execution cadence. This is operational discipline. It is unglamorous. It is essential.

Then automate. Layer technology, integration, and eventually AI on top of a stable, documented, consistently executed foundation.

Companies that skip standardization and go straight to automation do not get automated finance. They get faster versions of the same inconsistencies they had before. Operational discipline is the bridge between having good infrastructure and being able to use it.

Where to Start

Most companies do not know the full extent of their operational discipline gaps until they look carefully. The risks tend to be quiet. They surface during audits, during leadership transitions, and during periods of rapid growth when the informal processes that held at one size stop holding at the next. The

FSRA will give you a clear picture of where your operational discipline stands across the five pillars in about fifteen minutes.

Ted Rose

In 1994 Ted Rose founded Rose Financial Solutions (ROSE), the Premier U.S. Based Finance and Accounting Outsourcing Firm. In 2010, the Blackbook of Outsourcing named ROSE the #1 FAO firm in the world based on client satisfaction. As the president and CEO of ROSE, he provides executives with financial clarity. Ted has also acted as the CFO for a number of growth companies and assisted with various rounds of financing and M&A transactions.

Share this article:

Visit Us On: